Preface

Acknowledgements

Chapter 1: Introduction

Part One: Background Topics

Chapter 2: Important Finance Concepts

Chapter 3: Random Variables and Probability Distributions

Chapter 4: Inferential Statistics

PART TWO: FUNDAMENTALS OF SIMULATION, OPTIMIZATION, AND MACHINE LEARNING

Chapter 5: Simulation Modeling

Chapter 6: Optimization Modeling

Chapter 7: Optimization under Uncertainty

Chapter 8: Data and Data Science

Chapter 9: Regression Models

Chapter 10: Machine Learning

Chapter 11: Natural Language Processing

PART THREE: Applications to Asset Management

Chapter 12: Asset Allocation Models

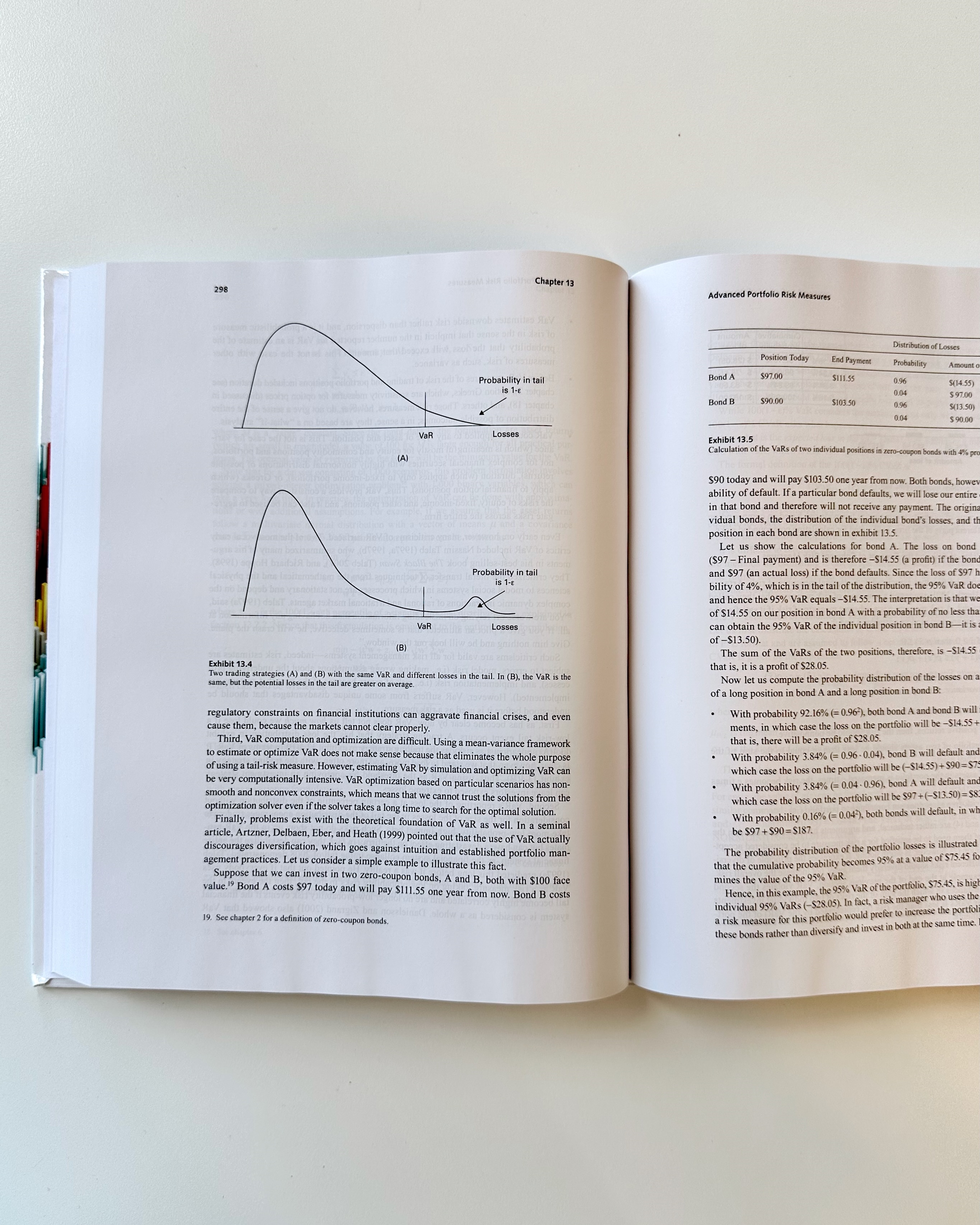

Chapter 13: Advanced Portfolio Risk Measures

Chapter 14: Equity Portfolio Selection in Practice

Chapter 15: Fixed Income Portfolio Management in Practice

PART FOUR: ASSET PRICING MODELS

Chapter 16: Factor Models

Chapter 17: Modeling Asset Price Dynamics

PART FIVE: FINANCIAL DERIVATIVES AND MORTGAGE-BACKED SECURITIES

Chapter 18: Introduction to Derivatives

Chapter 19: Pricing Derivatives with Simulation

Chapter 20: Using Derivatives in Portfolio Management

Chapter 21: Structuring and Pricing Residential Mortgage-Backed Securities

PART SIX: CAPITAL BUDGETING DECISIONS

Chapter 22: Capital Budgeting Under Uncertainty

Chapter 23: Application of Real Options to Capital Budgeting

Reference List